DOWNLOAD PDF

November 13, 2020

By Pierre Fréchette, Director of Research, CAAF

and Sherazade Shafiq, Program Officer, International Methodology and Training, CAAF

IntroductionAt the start of the COVID-19 pandemic, public sector auditors first had to adapt to working remotely and find ways to complete what they were working on when the crisis began. Then, once the initial shock subsided, many auditors started thinking beyond the short term to consider how their audit institution could adjust its audit plans to the new reality and provide information and assurance on the programs that governments created to provide much-needed support to citizens and businesses during the pandemic. In some cases, as in Canada (OAG Canada, 2020) and the United States (U.S. GAO, 2020), legislative bodies rapidly requested that auditors undertake audits of COVID-19 expenditures, and auditors agreed to do so. In other countries, such as the United Kingdom (NAO, 2020), the national audit office promptly started to produce reports to provide an overview of all the announced COVID-related programs and expenditures, thus helping parliamentarians and the public to keep track of spending. The Office of the Auditor General of British Columbia (2020) released a similar report in September 2020. But beyond preparing tallies of new expenditures and audits of how pandemic-related programs are managed, there is another way for auditors to be of service to their legislature: auditing government preparedness for future pandemics and providing assurance and actionable recommendations that will help public sector institutions achieve more effective responses during the next pandemic. This article presents an overview of what pandemic preparedness entails and of the work that performance auditors have done on this topic in the past. Specifically, it provides some answers to the following key questions:

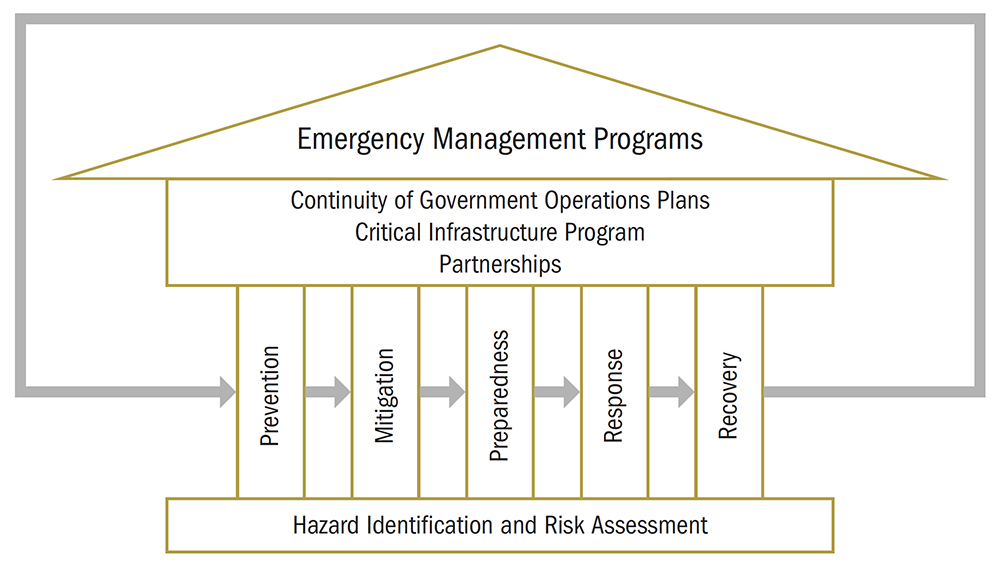

Emergency management and pandemic preparednessGovernments do not know when or where natural disasters such as earthquakes, droughts, floods, hurricanes, wildfires, or pandemics will occur, but they can always take steps to prepare for such emergencies and ensure that they are ready to respond effectively when they happen. Emergency management activities can be divided in five main categories:

Each category is essential to an effective emergency management program and must be supported by a solid assessment of the risks presented by each type of emergency (Figure 1). This article focuses on preparedness for pandemics. Preparedness, one of the five categories of emergency management activities in the above model, refers to actions taken to ensure there is sufficient capability and capacity to respond quickly and effectively to emergencies and to recover more rapidly from their long-term effects (Public Safety Canada, 2015). A pandemic is the worldwide spread of a new disease (WHO, 2010). Pandemic preparedness therefore refers to the actions taken by governments to ensure they can respond quickly and effectively when a new disease spreads around the world.

Key elements of pandemic preparedness include:

While many elements of pandemic preparedness, such as having response plans, are common to all kinds of disasters, from hurricanes to earthquakes, pandemic preparedness focuses particularly on preparedness in the health care sector. There is a special emphasis on the availability of personal protective equipment and medical equipment, surge capacity in medical institutions, and contagious disease monitoring and early warning systems. Why audit pandemic preparedness?As we have all learned in the COVID-19 crisis and, to a lesser extent, during the SARS pandemic in 2003, pandemics are not only deadly, but they can also have far-reaching socio-economic consequences for millions of Canadians. These consequences, both personal and societal, will be exacerbated in situations where the response to a pandemic is slow, uncoordinated, and made difficult by a lack of skills, medical supplies, and emergency budgets. Conversely, a fast, well-coordinated, and well-resourced response by trained and ready personnel can effectively limit the extent and consequences of a pandemic, as well as favour a more rapid recovery and return to normal life after the event. Ultimately, preparedness can save lives; prevent businesses from going bankrupt; limit disruptions for individuals; and significantly reduce the amount of fear, stress, and anxiety felt during a pandemic (INTOSAI, 2019a). By auditing pandemic preparedness, providing assurance, and making recommendations for improvement, public sector auditors can play an important role in ensuring that governments take adequate steps and allocate sufficient and adequate resources to prepare for and deliver an effective response to the next pandemic. Auditors can help reduce the impact of the next pandemic on citizens and communities. Auditing pandemic preparedness is also a good way to remind governments, parliamentarians, and citizens of the importance of preparedness activities. Through regular reports on preparedness, auditors may help governments to remain vigilant and ready, even when no outbreak has happened in many years and the risk of a pandemic may seem distant compared with more immediate concerns. Auditing pandemic preparedness: Past reports, current guidance, and considerations for future auditsAuditors seeking to undertake new audits of pandemic preparedness will naturally want to know whether and how this topic has been audited in the past and whether there is relevant guidance to help them audit it. We have researched these questions and present our findings on past audit reports and current guidance. We also highlight key considerations that auditors should take into account when planning to audit pandemic preparedness. Past audit reportsIt has long been known that a pandemic can strike at any time and that the consequences of such an event can be dramatic. Indeed, just a year before COVID-19 hit Canada, the Director-General of the World Health Organization reminded the world that “The threat of pandemic influenza is ever-present (…). The question is not if we will have another pandemic, but when. We must be vigilant and prepared – the cost of a major influenza outbreak will far outweigh the price of prevention” (WHO, 2019). Since the threat posed by pandemics is a constant, we could assume that public sector audit offices would regularly publish audits on pandemic preparedness2. However, our research did not support this assumption. In the pre-COVID period, we found few performance audit reports that focused on pandemic preparedness. Those we did find—from Canada, the United States, and Australia—were mostly released between 2007 and 2009 (Table 1). After 2009, very few audits on this topic are available online and almost all of those we could find were produced by the U.S. Government Accountability Office (GAO)3. A 2020 study of English-speaking African countries similarly found that a considerable number of national audit offices had not conducted any pandemic preparedness audits over the previous seven years (AFROSAI-E, 2020).

One hypothesis to explain the lack of recent pandemic preparedness audits is that such audits were conducted in the wake of the 2003 SARS pandemic and the avian flu (H5N1) scare from 2005 to 2007, but that preparedness mostly fell off the radar of audit offices when no new pandemic materialized over the following decade. Over the last decade, most audit offices moved away from pandemics as a topic and addressed preparedness only as part of more general audits on emergency management. (See Appendix A for a list of 14 Canadian audit reports on emergency management published between 2009 and 2019.) Only with the emergence of COVID-19 have audit institutions once again turned their attention to pandemics and preparedness. For example, a June 2020 report by the Controller and Auditor-General of New Zealand on the management of personal protective equipment looked at several preparedness aspects, including planning, guidelines, and supply stock management (Controller and Auditor-General of New Zealand, 2020). While most of the available audit reports on pandemic preparedness are now more than a decade old, they remain relevant and can be helpful for auditors interested in auditing this topic today. Most of these reports were focused on flu preparedness, but their methodologies could be adapted to other contagious diseases, including COVID-19. Current guidanceBesides consulting past audit reports, auditors interested in pandemic preparedness will likely want to read audit guidance on the topic. Unfortunately, they will find that few guidance documents existed before the current pandemic. In 2013, the International Organization of Supreme Audit Institutions (INTOSAI) released ISSAI 5510, The Audit of Disaster Risk Reduction (INTOSAI, 2013), which covered some aspects of preparedness for disasters in general. However, in 2018, INTOSAI undertook to review this guidance and at the time of writing was preparing a new guidance document. An exposure draft was released in May 2020 (INTOSAI, 2020a) and a consultation period ran until August 2020 (INTOSAI, 2020b). The new document, known as GUID 5330, was expected to be released in the near future. As part of its review work, INTOSAI conducted a research project on disaster preparedness for supreme audit institutions and published a document of the same name in 2019 (INTOSAI, 2019a). This document is a useful resource for auditors because it provides an overview of the various components of preparedness, presents options for audit scoping as well as case studies, and includes a section specific to disease outbreaks. In 2018, the British Columbia Auditor General for Local Government also published a useful resource on emergency management that includes information about the many elements of preparedness that are relevant for local governments (Auditor General for Local Government, British Columbia, 2018). More recently, in response to the COVID-19 pandemic, various organizations, including INTOSAI, have published articles, tools, and advice for auditors on various aspects of pandemic management. (These resources have been collected and can be found on the INTOSAI COVID-19 Initiative website and on the CAAF COVID-19 Resources Repository.) However, most of these resources are concerned with how governments and auditors are responding to the current crisis, as opposed to auditing pandemic preparedness per se. Considerations for future auditsFaced with the task of planning an audit on pandemic preparedness, auditors will quickly grasp some scoping options. Should the audit focus on whether the legal requirements set out in an Emergency Management Act or similar legislation have been implemented? Alternatively, should it focus on one or several key elements of preparedness, such as management of medical supply stockpiles, coordination mechanisms, surge capacity plans, and early warning systems, and determine whether current systems and practices meet international best practices? (This was done in the audit of outbreak preparedness and management by the Office of the Auditor General of Ontario, 2007.) Should the audit focus mostly on health institutions or on another key risk area (as in the audit of air travel and communicable diseases by the U.S. GAO, 2015)? But beyond those high-level scoping decisions, some important factors may not be as obvious and could be neglected during the audit planning process. These factors have to do with the populations at risk and how some groups may be more vulnerable to the health, social, and economic impacts of pandemics than others. It is widely recognized that inequalities have been growing around the world recently (UN DESA, 2020), and that those inequalities have been accentuated by the COVID-19 pandemic. There are indications that inhabitants of deprived areas and people already disadvantaged by poverty or disability have been the most affected by the coronavirus (OECD, 2020; Accounts Chamber of the Russian Federation, 2020). In addition, in Canada and other countries, women, visible minorities, and young people have borne the brunt of job losses and economic hardship brought about by the temporary closure of many economic sectors (Canada, 2020; Artuso, Mager, and Macías-Aymar, 2020). There have also been concerns expressed over the potential increase in violence against women during the required periods of confinement (UN Women, 2020a). (Previous studies have established that this type of violence increases during disasters; International Red Cross and Red Crescent Societies, 2015.) Governments should ensure their pandemic preparedness plans mitigate the potential adverse effects on disadvantaged groups. By understanding how vulnerable groups can be especially impacted by a pandemic (Regional Risk Communication and Community Engagement Working Group, 2020) and including specific audit questions on this aspect in their audit plans on pandemic preparedness, performance auditors can ensure that they are covering key risk areas. They will also be providing observations and recommendations that will help governments protect vulnerable groups during difficult circumstances (Bérubé and Schirnhofer, 2020; UN Women, 2020b; INTOSAI, 2013). (The Auditor General of Manitoba was conducting a performance audit on supports to vulnerable populations during the COVID-19 pandemic that will include some preparedness elements; OAG Manitoba, 2020.) Finally, another important consideration for auditors interested in tackling pandemic preparedness is whether they want to do it alone or collaborate with like-minded auditors in neighbouring jurisdictions. In recent years, cooperation among audit institutions around the world has increased considerably, especially on issues that are not constrained by administrative boundaries, such as air pollution, water protection, biodiversity conservation, and climate change6. As was made abundantly clear by COVID-19, pandemics also care little about boundaries and, based on this criterion, would be an adequate topic for collaborative audits. After all, neighbouring governments face similar threats from pandemics and would all benefit from having stronger plans to respond to the next pandemic. Similarly, auditors working together on pandemic preparedness could benefit from sharing ideas, knowledge, audit plans, and resources. Also, by reporting together, or in separate reports spread over a short period of time, audit institutions can increase their impact by raising the profile of the issues they report and their related recommendations (Leach, 2019). Auditors interested in a collaborative audit should consult the 2019 lessons learned report7 produced by the Office of the Auditor General of Canada after the 2018 pan-Canadian climate change audit8, the largest collaborative performance audit ever undertaken by legislative auditors in Canada. ConclusionThe threat of a new pandemic is ever-present and governments should remain vigilant and well-prepared to respond to the next outbreak. Public sector auditors can play an important role in ensuring that governments remain vigilant by regularly auditing pandemic preparedness. The COVID-19 pandemic has focused auditors on this topic and many lessons are now being learned and shared across the profession. By leveraging this new knowledge and experience, performance auditors will be better equipped to audit pandemic preparedness.

|

Appendix A – Canadian Performance Audit Reports on Emergency Management Published Between 2009 and 2019

| Year | Audit Office | Title |

| 2009 | Office of the Auditor General of Canada (OAG Canada) | Emergency Management – Public Safety Canada |

| 2013 | OAG Canada | Emergency Management on Reserves |

| 2014 | Office of the Auditor General of British Columbia | Catastrophic Earthquake Preparedness |

| 2015 | Provincial Auditor of Saskatchewan | Government Relations – Coordinating Emergency Preparedness |

| 2016 | Auditor General of Newfoundland and Labrador | Fire and Emergency Services |

| 2017 | Office of the Auditor General of the City of Ottawa | Emergency Preparedness and Response for Health Services |

| 2017 | Office of the Auditor General of Ontario | Emergency Management in Ontario |

| 2018 | Auditor General for Local Government of British Columbia (AGLG) | Emergency Management in Local Governments – Capital Regional District |

| 2018 | Vérificateur général de la ville de Trois-Rivières [Auditor General of the City of Trois-Rivières] | Mesures de sécurité civile et plan d’urgence [Public security measures and emergency plan] (French only) |

| 2018 | AGLG | Emergency Management in Local Governments – Town of Sidney |

| 2019 | AGLG | Emergency Management in Local Governments – Fraser Valley Regional District |

| 2019 | AGLG | Emergency Management in Local Governments – District of Mission |

| 2019 | Calgary City Auditor’s Office | Emergency Management Audit |

| 2019 | City of Edmonton Office of the City Auditor | Emergency Management Governance and Risk Assessment |

References

Accounts Chamber of the Russian Federation (2020). Social Impact of the COVID-19 Pandemic and Inclusion. Moscow: Author, available at https://incosai2019.ru/en/documents/52?download=298

AFROSAI-E (2020). Pocket Guide for Supreme Audit Institutions: Considerations on Responses to Disaster Situations, available at https://afrosai-e.org.za/2020/11/13/pocket-guide-for-sais-considerations-for-responses-to-disasters/?fbclid=IwAR37UvyAwQyz2lh7QvVPWNyxIMXeXPJ9RsxtxEYUhw2lNFo2oY32Ms2ndwM

Artuso, F., F. Mager, and I. Macías-Aymar (2020). “The COVID Inequality Ratchet: How the Pandemic Has Hit the Lives of Women, Minority and Poor Workers the Hardest.” OXFAM blog, available at https://oxfamblogs.org/fp2p/the-covid-inequality-ratchet-how-the-pandemic-has-hit-the-lives-of-young-women-minority-and-poor-workers-the-hardest/

Auditor General for Local Government (British Columbia) (2018). Improving Local Government Emergency Management. Surrey, BC: Author, available at http://www.aglg.ca/app/uploads/sites/26/2018/04/Perspectives-Series-Booklet-Improving-Local-Government-Emergency-Management.pdf

Bérubé, M.-H. and P. Schirnhofer (2020, summer). COVID-19: Putting a Gender Lens on Auditing. INTOSAI Journal of Government Auditing, available at http://intosaijournal.org/covid19-gender-lens-on-auditing/

Canada (2020). A Stronger and More Resilient Canada: Speech from the Throne to Open the Second Session of the Forty-third Parliament of Canada. Ottawa: Government of Canada, available at https://www.canada.ca/content/dam/pco-bcp/documents/pm/SFT_2020_EN_WEB.pdf

Controller and Auditor-General of New Zealand (2020). Ministry of Health: Management of Personal Protective Equipment in Response to COVID-19. Wellington, New Zealand: Author, available at https://oag.parliament.nz/2020/ppe/docs/ppe.pdf

International Organization of Supreme Audit Institutions (INTOSAI) (2013). ISSAI 5510 – The Audit of Disaster Risk Reduction. Copenhagen: INTOSAI Professional Standards Committee, available at https://www.environmental-auditing.org/media/5767/issai-5510-e.pdf

International Organization of Supreme Audit Institutions (INTOSAI) (2019a). Disaster Preparedness for Supreme Audit Institutions. INTOSAI Community Portal, available at https://www.intosaicommunity.net/document/exposure_draft/Draft_Final_Paper-RP_on_Auditing_Emergency_Preparedness.pdf

International Organization of Supreme Audit Institutions (INTOSAI) (2019b). GUID 9000 – Cooperative Audits Between SAIs, available at https://www.intosaicbc.org/wp-content/uploads/2020/05/GUID-9000-Cooperative-Audits-between-SAIs-1.pdf

International Organization of Supreme Audit Institutions (INTOSAI) (2020a). GUID 5330 Exposure Draft – Guidance on Auditing Disaster Management, available at https://www.issai.org/wp-content/uploads/2019/08/Guid-5330-Exposure-Draft.pdf

International Organization of Supreme Audit Institutions (INTOSAI) (2020b). “New Exposure Drafts on GUID 4900 and GUID 5330 Ready for Comments at ISSAI.ORG until August 27, 2020.” INTOSAI Community Portal, available at https://www.intosaicommunity.net/user/newsdetails/66

International Red Cross and Red Crescent Societies (2015). Unseen, Unheard: Gender-based Violence in Disasters – Global Study. Geneva: Author, available at https://www.ifrc.org/Global/Documents/Secretariat/201511/1297700_GBV_in_Disasters_EN_LR2.pdf

Leach, K. (2019). Collaborative Climate Change Audit Project: Process Chronicle and Lessons Learned. Ottawa: Office of the Auditor General of Canada, available at https://www.caaf-fcar.ca/images/pdfs/performance-audit/ExternalPublications/CollaborativeClimateChangeReport-LessonsLearnedEN.pdf

Lutes, K. (2019). Lessons Learned from the Pan-Canadian Climate Change Audit – 2016-2018. Ottawa: Canadian Audit and Accountability Foundation, available at https://www.caaf-fcar.ca/en/performance-audit/audit-news/featured-audits/3468-featured-audits-6

Office of the Auditor General of British Columbia. (2020). Summary of COVID-19 Pandemic Funding Allocations and Other Financial Relief Measures. Victoria, BC: Author, available at https://www.bcauditor.com/pubs/2020/summary-covid-19-pandemic-funding-allocations-and-other-financial-relief-measures

Office of the Auditor General of Canada (OAG Canada) (2018). Perspectives on Climate Change in Canada. Ottawa: Author, available at http://publications.gc.ca/collections/collection_2018/bvg-oag/FA3-137-2018-eng.pdf

Office of the Auditor General of Canada (OAG Canada) (2020). Opening Statement to the Standing Committee – Government’s Response to the COVID-19 Pandemic. Ottawa: Author, available at https://www.oag-bvg.gc.ca/internet/English/osh_20200512_e_43563.html

Office of the Auditor General of Manitoba (OAG Manitoba) (2020). Audits in Progress. Winnipeg: Author, available at https://www.oag.mb.ca/audit-reports/in-progress/

Office of the Auditor General of Ontario (2007). Outbreak Preparedness and Management. Toronto: Author, available at https://www.auditor.on.ca/en/content/annualreports/arreports/en07/312en07.pdf

Office of the Auditor General of Ontario (2017). Emergency Management in Ontario. Toronto: Author, available at https://www.auditor.on.ca/en/content/annualreports/arreports/en17/v1_304en17.pdf

Organisation for Economic Co-operation and Development (OECD) (2020). The Territorial Impact of COVID-19: Managing the Crisis Across Levels of Government. Paris: Author, available at https://www.oecd.org/coronavirus/policy-responses/the-territorial-impact-of-covid-19-managing-the-crisis-across-levels-of-government-d3e314e1/

Public Health Ontario (2020). Public Health Emergency Preparedness Framework and Indicators. Toronto: Author, available at https://www.publichealthontario.ca/-/media/documents/w/2020/workbook-emergency-preparedness.pdf?la=en

Public Safety Canada (2015). “Emergency Management Planning – Frequently Asked Questions,” available at https://www.publicsafety.gc.ca/cnt/mrgnc-mngmnt/mrgnc-prprdnss/mrgnc-mngmnt-plnnng-faq-en.aspx

Public Safety Canada (2017). An Emergency Management Framework for Canada, Third Edition. Ottawa: Author, available at https://www.publicsafety.gc.ca/cnt/rsrcs/pblctns/2017-mrgnc-mngmnt-frmwrk/2017-mrgnc-mngmnt-frmwrk-en.pdf

Regional Risk Communication and Community Engagement Working Group (2020). “COVID-19: How to Include Marginalized and Vulnerable People in Risk Communication and Community Engagement,” available at https://interagencystandingcommittee.org/system/files/2020-03/COVID-19 - How to include marginalized and vulnerable people in risk communication and community engagement.pdf

United Kingdom National Audit Office (NAO) (2020). “Overview of the UK Government’s Response to the COVID-19 Pandemic,” available at https://www.nao.org.uk/press-release/overview-of-the-uk-governments-response-to-the-covid-19-pandemic/

UN Women (2020a). “The Shadow Pandemic: Violence Against Women During COVID-19,” available at https://www.unwomen.org/en/news/in-focus/in-focus-gender-equality-in-covid-19-response/violence-against-women-during-covid-19

UN Women (2020b). “Rapid Guide – Gender, COVID-19 and Audit,” available at https://www.unwomen.org/-/media/headquarters/attachments/sections/library/publications/2020/rapid-guide-gender-covid-19-and-audit-en.pdf?la=en&vs=1231

United Nations Department of Economic and Social Affairs (UN DESA) (2020). Inequality in a Rapidly Changing World – World Social Report 2020. New York: Author, available at https://www.un.org/development/desa/dspd/wp-content/uploads/sites/22/2020/01/World-Social-Report-2020-FullReport.pdf

U.S. Government Accountability Office (U.S. GAO) (2015). Air Travel and Communicable Diseases: Comprehensive Federal Plan Needed for U.S. Aviation System’s Preparedness. Washington, DC: Author, available at https://www.gao.gov/products/GAO-16-127

U.S. Government Accountability Office (U.S. GAO) (2020). Coronavirus Oversight. Washington, DC: Author, available at https://www.gao.gov/coronavirus/

World Health Organization (WHO) (2010). “What Is a Pandemic?,” available at https://www.who.int/csr/disease/swineflu/frequently_asked_questions/pandemic/en/

World Health Organization (WHO) (2019). “WHO Launches New Global Influenza Strategy,” available at https://www.who.int/news-room/detail/11-03-2019-who-launches-new-global-influenza-strategy

Endnotes

1 In some emergency management frameworks, prevention and mitigation are combined in a single category, as in Public Safety Canada’s 2017 Emergency Management Framework for Canada.

2 Admittedly, this reasonable idea operates on the assumption that auditors should regularly audit all important risks; in reality, audit budgets are limited and choices must be made among multiple priority topics.

3 We searched the CAAF Audit News Database, as well as generic online search engines. We mostly restricted our search to English reports, although we did search the French reports produced by the Auditor General of Québec and by several municipal audit offices in the province of Quebec. We focused our search on the 2000 to 2020 period.

4 This is a summary report covering 11 reports published by the U.S. GAO from 2007 to 2009, which are listed in the summary report.

5 This audit looked at an IT system intended to provide public health officials and staff across Canada with the real-time ability to collect, share, and analyze health information critical for managing infectious disease outbreaks.

6 An extensive list of cooperative audits is available in INTOSAI’s GUID 9000 – Cooperative Audits Between SAIs (INTOSAI, 2019b).

7 Leach, 2019. For a short summary of the lessons learned, see CAAF’s 2019 Featured Audit edition Lessons Learned from the Pan-Canadian Climate Change Audit – 2016-2018 (Lutes, 2019).

8 Each jurisdiction published its own audit report and a joint summary report was prepared to conclude the audit project. See OAG Canada (2018), Perspectives on Climate Change in Canada.

See more Research Highlights