Oversight Bodies

In general terms, an oversight body is a group of people with a common oversight purpose acting as an organized unit. In this Practice Guide, emphasis is put on oversight bodies that have:

- a discrete structure,

- a degree of independence, and

- a clear oversight mandate.

An oversight body may also be an organization’s governance body (a board of directors, for example), or it may be a committee or other structure that reports directly to the governance body (an audit committee, for example).

The board of directors of a Crown corporation, the governing body of a local health or education authority, and a regulatory board for a specific economic sector would all meet the definition of an oversight body. However, the Practice Guide recognizes that it is possible to audit oversight even when some of these conditions (discrete structure, independence, and clear mandate) are not met. While some sections of the Practice Guide may be less applicable in such cases, other sections will be easily adaptable.

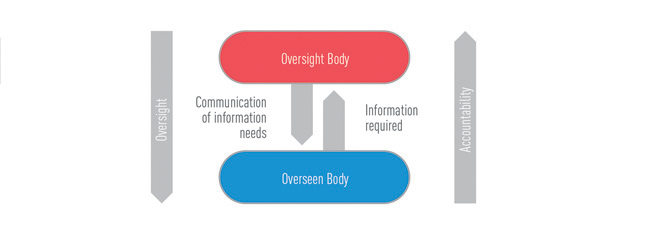

Each oversight body has its own unique characteristics. What unites oversight bodies is the nature of their relationship with their overseen organization and the oversight functions they play. As shown in Figure 8, the relationship between oversight bodies and overseen bodies is mediated through the exchange of information from one body to the other. The oversight body communicates its information needs to the overseen body and the latter provides the required information in return, thus fulfilling its accountability obligation.

Figure 8

Information Flow Between Oversight and Overseen Bodies

This exchange of information can take place at more than one level. Depending on reporting relationships, an organization may report to a second organization (a regulatory agency or a health authority, for example), which itself reports to a third organization (a department or Parliament/legislature). In this case, the second organization is both an oversight body (overseeing the first organization) and an overseen body (overseen by the third organization).

The expression “oversight of oversight” can be used to describe such situations where an oversight body oversees another oversight body. Figures 4, 5, and 6 each illustrate examples of oversight of oversight. In Figure 4, for example, the Regional Health Authorities are both oversight bodies and overseen bodies. Note, however, that the oversight relationships illustrated in these diagrams are not necessarily hierarchical; some are horizontal.

The role of “oversight of oversight” is an important one, especially where ministers are responsible for overseeing agencies, boards or authorities. This was recognized by Ontario’s Standing Committee on Public Accounts in its 2014 report on the Ornge air ambulance service:

“The Committee notes that the events at Ornge confirm that it is not responsible simply to rely on the boards of transfer agencies to provide appropriate oversight. The Ministry must exercise its responsibility to ensure that public funds are being properly administered and that boards are held accountable for their actions.”

In recent years, many audits have reported significant weaknesses in the oversight of certain agencies, boards or authorities by their responsible minister. Examples include the 2011 New Brunswick audit of the oversight of wastewater commissions, the 2009 Ontario audit of the Electronic Health Records initiative, and the 2012 Ontario audit of the Ornge air ambulance service.

Audits can therefore look at oversight at different levels within a single audit:

- oversight by a board or another body of an organization’s activities,

- oversight of this board or body by its responsible minister, and

- oversight of the organization’s activities by an independent regulatory agency.