Background

Since its creation in 1980, the CCAF (now the Canadian Audit and Accountability Foundation) has worked closely with the Canadian Council of Public Accounts Committees (CCPAC) to develop innovative means to strengthen Canada’s PACs and enhance cooperation between PACs and the legislative auditors.

Our first major research project was to examine the role and function of Canadian Public Accounts Committees and legislative auditors. In 1981, we published a report on Improving Accountability: Canadian Public Accounts Committees and Legislative Auditors. In 1989, CCPAC published a series of guidelines for a model Public Accounts Committee in Canada. Many other studies and resources for PACs have followed.

Our first major research project was to examine the role and function of Canadian Public Accounts Committees and legislative auditors. In 1981, we published a report on Improving Accountability: Canadian Public Accounts Committees and Legislative Auditors. In 1989, CCPAC published a series of guidelines for a model Public Accounts Committee in Canada. Many other studies and resources for PACs have followed.

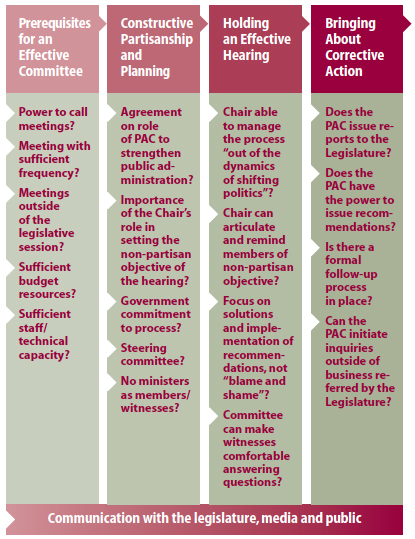

More recent studies and products have assessed trends in PAC effectiveness and set out good practices to strengthen PAC capacity. We based our 2006 “Guide to Strengthening Public Accounts Committees” on the findings of a survey of the 14 Canadian PACs conducted in 2004. On the basis of the 2004 survey and the 2006 PAC Guide, we developed a model for “An Effective Public Accounts Committee.” Since 2006, we have used and adapted this model for numerous PAC orientations and other other workshops in Canada (see figure below).

In 2007, CCPAC asked us to develop a vision for a ‘PAC of the Future’, comprising key concepts to guide the PAC ten years hence. (See text box below.)

|

We presented three key concepts for ‘The PAC of the Future’ at the Annual joint meeting of the Canadian Council of Public Accounts Committees and the Canadian Council of Legislative Auditors in 2007

|

A Model for an Effective Public Accounts Committee

In 2008, in cooperation with KPMG and the World Bank Institute, we conducted a survey of PAC practices in Canada. The results, presented at the annual joint meeting of CCPAC and the Canadian Council of Legislative Auditors (CCOLA) in 2008 in Whitehorse, provided a snapshot of current PAC activity across Canada. The results also highlighted certain trends, issues and challenges for PACs in Canada.

At the Whitehorse meeting, some CCPAC members proposed that CCAF develop a brief, concise and easily accessible document to consolidate the key themes and issues regarding PACs that have emerged:

- The cutting edge practices of PACs in Canada;

- Recent thinking about PAC practices (i.e. the role of the PAC in communicating value-added);

- Recent trends and developments.

At the request of CCPAC, we agreed to outline the characteristics or attributes of an effective PAC and facilitated the development of a draft version of the Attributes for discussion at the 2009 CCPAC-CCOLA conference in Edmonton. We based this draft on previous studies, surveys, presentations and reports for CCPAC, as well as discussions with CCPAC and its members. In addition, we reviewed research on PACs conducted by the World Bank Institute and others.

In 2013, we conducted a new survey of Canada’s fourteen PACs and presented the results to the annual meeting of CCPAC-CCOLA in Regina in August. In 2014, we updated the Canadian Landscape and Practice Highlights for each of the twelve Attributes based on the new survey data and interaction with PACs across Canada. In some cases, Practices to consider were also updated.

The Attributes should be relevant to all Canadian jurisdictions. However, different political and institutional realities may impede the adoption of all practices uniformly. Some jurisdictions might find a particular practice desirable but not feasible. Feasibility can be influenced by such factors as the timing of an electoral cycle, the structure of the committee system, resource availability, whether a government has a majority or minority in the legislature, and the existence of other potentially conflicting practices. Clearly, not every practice identified to achieve the Attributes will apply to every jurisdiction and practices will vary accordingly.

The 12 Attributes, prepared for discussion with the Canadian Council of Public Accounts Committees, cover the following: