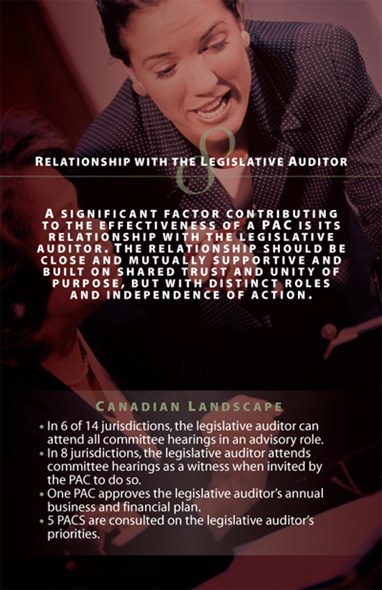

Relationship with the Legislative Auditor

Reliance on Independent Information

PACs require credible and independent information to carry out their duties in overseeing the implementation of government policy.

Practices to Consider

- Rely on the legislative auditor’s attest audit of the public accounts.

- Rely on the legislative auditor’s audit reports as a credible source of independent information on the government’s administration of programs.

Cooperation with and Support for the Legislative Auditor

PAC effectiveness can be optimized if the PAC and the legislative auditor cooperate and are able to support each other. Other legislative committees may also play a role in supporting the legislative auditor.

Practices to Consider

- Meet annually with the auditor to review plans, provide input to the audit office’s work plan (where desirable), and discuss any concerns the PAC or the legislative auditor might have.

- Play a role in addressing concerns regarding mandate, resources, access to information and independence of the legislative auditor.

- Invite the legislative auditor to be present during meetings or hearings, whether the legislative auditor is acting in an advisory capacity or as a witness to the PAC.

- Ask the legislative auditor to brief the PAC in advance of committee hearings on the legislative auditor’s reports.

- Invite the legislative auditor to make opening statements and concluding remarks at committee meetings.

- Work closely with the legislative auditor to follow up on recommendations of the auditor and the PAC.

Practice Highlights

- In Prince Edward Island, Nova Scotia and Alberta, the estimates of the legislative auditor are reviewed by a legislative committee other than the PAC.

- In BC, the Select Standing Committee on Finance and Government Services reviews and approves the Auditor General’s three-year service plans and annual reports.

- In Manitoba, the Auditor General has raised concerns related to the lack of delegated staffing authority.

- In PEI, the Legislative Audit Committee is mandated to provide guidance to the Auditor General on how to resolve matters of conflict affecting their independence and effectiveness.

- The Auditor General of Nova Scotia has appeared before the PAC regarding denial of access to certain documents during the course of an audit. The PAC responded by issuing subpoenas.